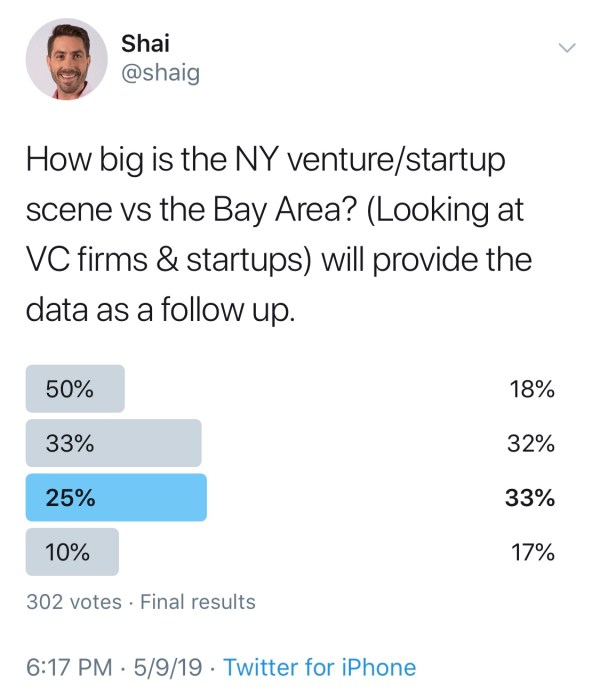

I sent out this tweet survey and got a lot of responses , so this blog post is to provide the actual answer and the underlying data.

The tldr is that NY Metro tech scene is 50% the size of the Bay Area tech scene, I’m sure you might be surprised or skeptical, just hear me out. 18% of the twitter survey respondents got it right.

The correct answer to the survey really depends on what data you are analyzing and comparing, so really all the twitter survey responses COULD be accurate , it is all about how you slice & dice it.

For the data gathering, I used two publicly available (you need subscriptions) data sources , PitchBook and CB Insights, which are my favorite tools for startup/VC information.

Now this isn’t about NYC vs SF but a bit broader NY Metro vs Bay Area, is captures the full startup scene as comparing distinct cities isn’t comprehensive. Example , there are startups in Palo Alto, Oakland and Jersey City, these are examples of other cities need to be included in a comparison.

I looked at startups and VC firms to measure the tech community. Both the startups and VC firms had to be HQ’d in the respective regions that I’m comparing. I wanted to look at data that was more a leading indicator (early stage companies) as opposed to a lagging indicator (late stage / public companies). I believe that looking at early stage companies will give us a better sense of where these respective markets are headed and the potential they hold.

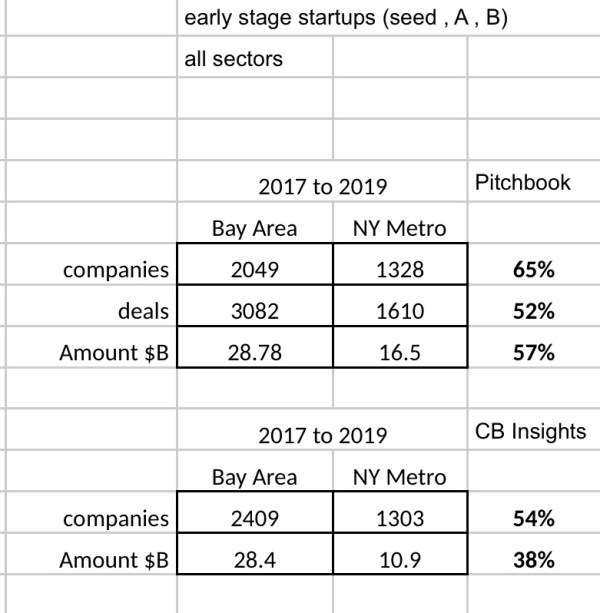

For the startup side, I reviewed the number of deals, the number of rounds and the aggregate amount of the funding. The time period was Jan 1st 2017 to May 9th 2019. The rounds of financing for the comparison was Seed, Series A and Series B. In terms of sectors, it was comprehensive, so life science, energy , consumer , enterprise , etc was included.

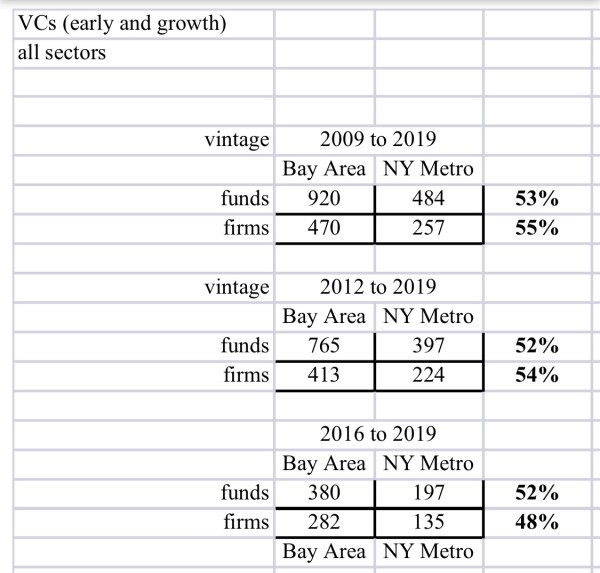

For the VC firms , I looked at funds that were raised between Jan 1st 2016 and May 9 2019. As you may have noticed , I used a slightly longer time period (one additional year) for VC funds, as some VC firms only raise capital once every three years, so wanted to capture all the relevant funds. The funds were both early and growth stage funds, similar to companies , included all funds regardless of sector focus (or geography focus). I also looked at the number of firms, which is distinct from the number of funds, although they are obviously related.

Here is the first piece of the data, which you can see includes some bonus data with expanded time horizons on the funds side.

Here is a visual on the number of VC firms, per PitchBook:

Here is the data on the company side, are you can see there is discrepancy between CB Insights and Pitchbook on the aggregate amount of funding but in terms of number of companies, they are similar.

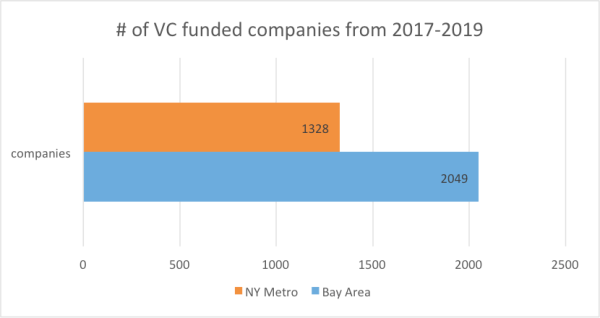

Here is a visual of number of VC funded companies via PitchBook.

So to summarize, I believe the NYC Metro scene is about half the size of the Bay Area startup scene (18% of the respondents to the twitter survey got that question right). I have never thought that the two metro regions would be equal in size but have mentioned before that I thought NY could be half the size, I’m really surprised it happened this quickly though.

If you have any comments or thoughts, please post or hit me up on twitter @shaig. Thanks for reading this far……