As you may of heard, Slack just raised a $200M round of financing at a $3.8B valuation.

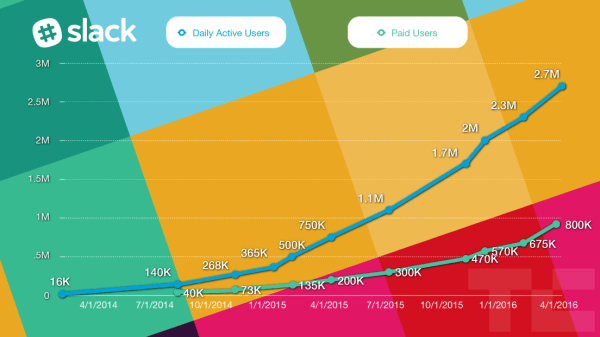

Per the first image below, they have 800K paying users.

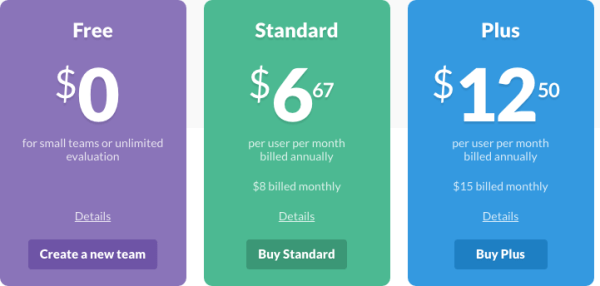

If you look further down at the second image, you can see how much they charge paying users, between $6.67 per month or $15 per month.

Assuming all their 800K paying users are at the lower tier of $6.67 per month, they are at $64M in annual recurring revenue ($6.67 x 12 months x 800K). If they were a public company at this revenue, they would be trading at a 60x revenue multiple ($3.8B/$64M).

If their 800K paying users were at the high tier of $15 per month, they are at $144M in annual recurring revenue and 26x revenue multiple ($3.8B/$144M).

Realistically, their users are paying somewhere in the middle of $6.67 and $15, so splitting the difference of 60x and 26x multiple, they would need to trade at a 42x multiple.

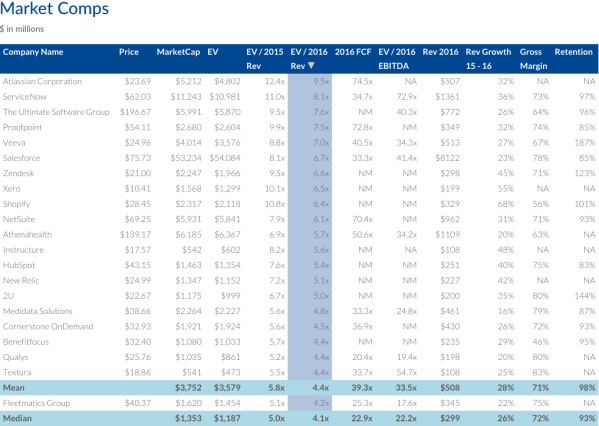

Taking a look at the Bessemer Cloud Index, you can see that the largest multiple of public saas companies is Workday, trading at a 10x revenue multiple. So assuming the best case scenario, Slack is getting paying users at the upper tier of $15/month, the 26x revenue multiple is much bigger than Workday’s. That being said and a major implication to their current valuation, they are growing at a much faster pace than Workday or any other company in the Cloud Index.

If you look at the valuation of companies in the Cloud Index, fourth image below, only 9 companies have a higher valuation than Slack’s $3.8B.

Given Slack’s revenue and growth rate, they could IPO today, but the big question is what their market capitalization could be.

Great writeup, Shai. My big question about Slack (I’m a user) is “stickiness”. I could quit using Slack tomorrow and my life wouldn’t change dramatically. Not the same for apps like Workday. I wonder if there’s a need to look at a “stickiness” axis as well, which might help establish a valuation floor.

for how long have you been using slack?

the longer you use it, the more history you have sitting there: valuable conversations, shared content/links, documented decisions etc.

like one uses to search email archives, you will turn to slack for reference.

so I would say there definitely is a lock-in…

Pingback: Mattermark Daily - Monday, April 4th, 2016 - Mattermark

Remember when Twitter was the poster boy of unicorns a. la Slack? Twitter’s timeline got noisy and people just stopped using it. Slack, in my opinion, is also facing a similar possibility with noisy channels, thanks to all their gif & other integrations.

This kinda of touches on what Timothy mentioned. What is Slack’s long term play? It’s a great product but how far can they go before they are acquired?

High growth startups attract investors that are willing to invest at a high revenue multiple (compared to public comps) with the belief that they will grow into the valuation. Jason Lemkin did a great episode of TWiST back in November that touches on this: http://thisweekinstartups.com/jason-lemkin-saastr/

Pingback: What You May Have Missed #VC #Startup – citizen.vc inc.

Pingback: Slack $7B valuation | Shai's Blog