As you may have heard, the venture market has cooled in 2016, in terms of dollars invested and number of investments (deals) that are being done by venture capitalists (VCs).

There are a number of reasons for why this has happened. The main driver has been the macro environment- forces that VCs can’t control. It is a combination of a slowdown in China, challenges with several European countries, Brazil, ISIS, volatility of oil prices, upcoming US election, etc. This in turn has created “bears” in the public markets, which has resulted in almost no VC backed IPOs and a correction in the SaaS sector as a result of the significant LinkedIn ($LNKD) price drop in February 4, 2016. The chain reaction of all of this has led to VCs becoming more cautious and spending additional time with their existing portfolio companies.

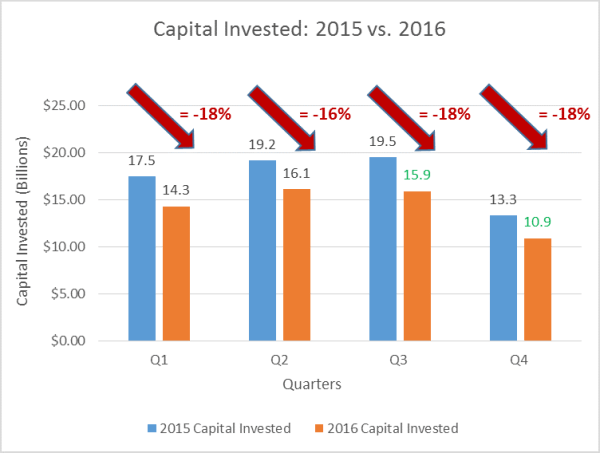

The data below was pulled via CBInsights. We analyzed deals/dollars in the US for 2016.

The most significant point is the drop of deals in Q2 ’16 vs Q2 ’15, a whopping 28% delta. We wanted to be predictive on what the 2nd half of this year would look like and it is a bit bearish. The figures in green are just guesses, so could be totally wrong here but wanted to be on the record on what I think will happen. The reasons on why the 2nd half may turn out to have a great delta between 2015 vs 2016 is that the markets are still facing significant macro issues, with the newest being #brexit, which has created additional uncertainty that will likely trickle down to the venture ecosystem.

There is good and bad news on the prediction. When you put the numbers of both 2015 and 2016 into context, they are really high compared to previous years, so a lot of deals and dollars are still being deployed, which is the good news. The bad news from an entrepreneur’s perspective, is that raising money from VCs has gotten a lot more difficult.

Now, lets focus our attention on the dollars deployed by VCs, see second image. Similar to deals, the numbers are down, although not as pronounced. What we are seeing is that round sizes have gotten slightly larger on average, which can be mean a few things. One it could mean that VCs are putting more money into their better companies (i.e. flight to quality) and/or the runways are being extended as the forecast of macro environment is uncertain.

Similar to the prediction of deals for the rest of the year, the numbers will likely be down, although not as significant.

Although the outlook is bearish, the reduced numbers in 2016 (vs 2015) is positive for the venture environment, as the market was over-heated and the correction was needed.

Thanks to our summer intern, Lorel Sim, for pulling this data.

Q3 and Q4 2016 data are only predictions (numbers in green).

Data was only for US based private tech (all sectors) companies.